Blog & Insights

Payment Portals: Electronic Payments and Card Fees – The Final Hurdle

This is part four of a four-part series about payment portals. Click to read part one, part two, and part three.

Lock and key. Bow and arrow. Thunder and lightning – just a few of the many things in this world that go hand in hand. When one is present, the other isn’t too far behind. There is a similar relationship with your payment portal – electronic payments and fees. Collection agencies have faced a myriad of challenges in the past when accepting electronic payments. While better today, these agencies still have many hurdles to address.

Past and present

Having worked in, and on behalf of, the banking, credit, and collection industries for more than 30 years, I have firsthand knowledge of the challenges third-party debt collectors have faced when seeking merchant status under the brand rules for companies, such as Visa and Mastercard.

Initially, the card brands shunned third-party debt collectors. It was difficult, if not impossible, to obtain merchant status. This was particularly problematic if the agency’s name revealed that it was a third-party collection agency. Agencies seeking merchant status needed to:

- Apply through third-party brokers

- Use acronyms or pseudonyms in place of the true name of their organization

- Describe their business in generic receivables management terms.

Worst of all, the card brands categorized these collection agencies as high-risk merchants. Therefore, the card brands charged agencies at least two to three basis points more than low-to-medium-risk merchants to process their card payments.

Fortunately, the industry and the card brands have evolved. Today, third-party debt collection agencies can freely and openly hold merchant status in the legal name of the organization. And they can accept credit, debit, Health Savings Account (HSA), and similar cards for payment of the debt. But ironically, the appeal of holding merchant status and accepting cards in payment of the debts subject to third-party collections has dwindled.

The processing costs associated with card payments have become prohibitive for third-party collection agencies for three reasons.

- The cards continue to consider third-party collection agencies as high-risk merchants. Therefore, they charge them a higher percentage to process their card payment transactions. This reduces the agencies’ margins on card payments.

- The unrelenting pressure that creditors place on third-party debt collection agencies to decrease their contingency fee further reduces the margins collection agencies make on consumer payments.

- The law prohibits third-party debt collectors, unlike all other merchants, from charging consumers any type of service fee, surcharge, convenience fee, or processing fee when accepting card payments on debt.

Follow the rules

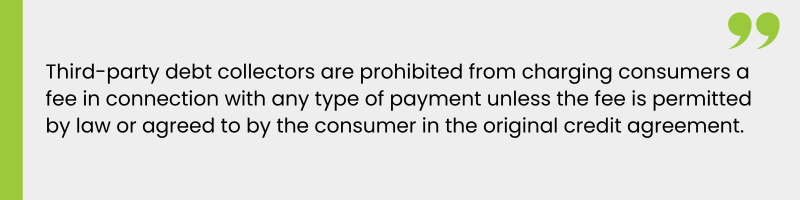

Third-party debt collectors are prohibited from charging consumers a fee in connection with any type of payment unless the fee is permitted by law or agreed to by the consumer in the original credit agreement.

For your reference, this prohibition is found in 15 USC 1692 f (1), the unfair practices section of the Fair Debt Collection Practices Act (FDCPA):

“A debt collector may not use unfair or unconscionable means to collect or attempt to collect a debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section… (1) The collection of any amount (including any interest, fee, charge, or expense incidental to the principal obligation) unless such amount is expressly authorized by the agreement creating the debt or permitted by law.”

This prohibition is unique to third-party debt collectors. It means they cannot add any fee to the amount they collect from a consumer – either directly or indirectly. This includes any type of processing fee, service charge, convenience fee, surcharge or independent card payment with a credit or debit card payment. Nor can a third-party debt collector contract with a card processing company that charges the consumer a fee for making the card payment and then provides the agency with a kickback or any form of remuneration.

As these processing charges are proving costly, more third-party debt collectors are no longer accepting credit or debit card payments from consumers. This, of course, is problematic for consumers who, quite often, have no alternative source of funds to pay their debt.

Recognizing the legal predicament third-party collectors face regarding the assessment of any type of fee in connection with card payments, and the overwhelming preference of consumers to make payments using their credit and debit cards, Finvi introduced the Technology Usage Fee (TUF) program. By enrolling in TUF, third-party collection agencies become authorized agents of Finvi.

Recognizing the legal predicament third-party collectors face regarding the assessment of any type of fee in connection with card payments, and the overwhelming preference of consumers to make payments using their credit and debit cards, Finvi introduced the Technology Usage Fee (TUF) program. By enrolling in TUF, third-party collection agencies become authorized agents of Finvi.

In this capacity, once a consumer asks to pay the agency using a card, either during a live call with the collection agent or on the collection agency’s portal, Finvi’s contract with the agency requires the collection agency to explain to the consumer that their agency no longer accepts card payments but that if the consumer so desires, they may make a card payment on their account using Finvi’s card processing technology.

Additionally, collection agencies must clearly state to their consumers any and all fees associated with making an online portal payment. This is to ensure that your organization is fully transparent and in compliance with local, state, and federal regulations. It is imperative that collections organizations:

- Clearly indicate if the fee is being charged by a party other than the debt collector

- Affirm that the fee is payable to a third-party payment processor

- Explicitly confirm the consumer’s agreement while offering an alternative free-of-charge option.

Some of these free-of-charge options come with limitations. These could be on the number of transactions, the amount of each transaction, or some other restriction. These must also be clearly identified to and acknowledged by the consumer.

Types of portal payments

Recurring payments are those payments that are processed on a predetermined schedule. These are a very common transaction type on most payment portals. Consumers appreciate the convenience of not having to remember when a payment is due. And they appreciate not having to log in each time. This convenience also leads to greater consumer retention. Collection agencies also receive a predictable cash flow from recurring electronic payments. However, the agency or the consumer may need to cancel these transactions for any number of reasons. The rules for doing so must be clearly defined for the consumer. One payment portal has the following rules depending on the method of payment:

- Scheduled and pre-authorized recurring payments/bank funds transfers: Electronic Funds Transfers (EFT) created by debit card or bank transfer must include specific Reg E disclosures to which the consumer must agree to in writing and sign, or agree to electronically and sign, per the requirements of the Electronic Signatures in Global Commerce Act.

- If your debit payment or bank funds transfer has already started processing, you will be unable to cancel the transaction. For scheduled and pre-authorized recurring payments or transfers that have not started processing, the consumer must cancel or edit the payment instructions at least three (3) business days before the scheduled payment/transfer date. If the consumer directs the agency to cancel a scheduled or preauthorized recurring payment/transfer at least three (3) business days before the payment is scheduled, and the agency does not, the agency will be liable for the customer’s losses or damages per the penalty provisions of the Electronic Funds Transfer Act and Regulation E.

- Credit card recurring payment arrangements do not require compliance with NACHA rules, the Electronic Funds Transfer Act (EFTA), or Regulation E. Credit card transactions must meet the requirements of the card brand rules.

Ready to go

Payment portals are a necessity for collections and recovery agencies. These portals can simplify the collections process, help increase recovery rates, and improve the consumer experience. Now you should be able to confidently research and implement the right payment portal for your organization.

Disclaimer: Finvi is a technology company and provides this post solely for general informational and marketing purposes. You should not rely on the content of this material for any other purpose or as specific guidance for your company. Finvi’s advice, services, tools, and products described herein do not guarantee compliance with any law or industry standard. You are ultimately responsible for your own company’s actions and compliance efforts. Because everyone’s situation is different, you must consult your own attorneys, accountants, and/or other advisors to obtain specific advice on your company’s compliance, legal, tax, regulatory and/or other business needs. Despite Finvi’s efforts to provide current and up-to-date information, you need to recognize that the information contained herein may become outdated quickly and may contain errors and/or other inaccuracies.

Rozanne Andersen

Rozanne M. Andersen is a distinguished attorney known for her expertise in compliance, particularly within the realms of collection, debt purchasing, and financial services. With a proven history of leadership and advocacy, she stands out as an industry luminary. Her comprehensive knowledge extends to association law, corporate governance, and providing general counsel services. Renowned as a national speaker, she shares her insights on critical legislation such as the Fair Debt Collection Practices Act, the Fair Credit Reporting Act, federal and state consumer protection regulations, and the Health Insurance Portability and Accountability Act. Currently, Rozanne serves as Risk and Compliance Consultant for Finvi, formerly known as Ontario Systems. Her unparalleled expertise helps Finvi remain at the forefront of compliance, enabling clients to navigate the intricate web of state and federal requirements seamlessly.